The great wealth transfer

What does the great wealth transfer mean for those who are set to inherit – and, importantly, for those looking to transfer their assets meaningfully?

Inheritances, particularly large ones, can be problematic. By their nature, they mean someone important to you has passed away.

As such, there can be an emotional burden around not misspending a loved one’s hard-earned wealth. Tensions can also arise between family members if there’s a perceived lack of equity, or if there’s a business involved. Then, of course, there are the complications of non-nuclear families where second partners or stepchildren may be involved too.

That’s why it’s vital to think carefully around how and when you transfer your assets – to lessen any distress and help you and your family remain financially secure into the future.

The need to succeed

It’s a salient issue. Michael Saadie, Head of NAB Private Wealth and CEO of JBWere, says this represents an important opportunity for individuals, families and businesses.

"We are about to see the largest wealth transfer in Australia’s history. By 2050, it’s estimated about $3.5 trillion in assets will change hands. Meanwhile, in the next five years around 70 per cent of privately owned Australian companies will gain new owners because the principal major shareholder is over 70 years of age."

Thousands of us will have to decide how best to share a lifetime of wealth and learn how to manage the transition of this wealth. This substantial transfer of capital will shape our fortunes as well as the economic and social make-up of our country.

Source: Vanguard, Preparing for the biggest wealth transfer in history

Source: Vanguard, Preparing for the biggest wealth transfer in history

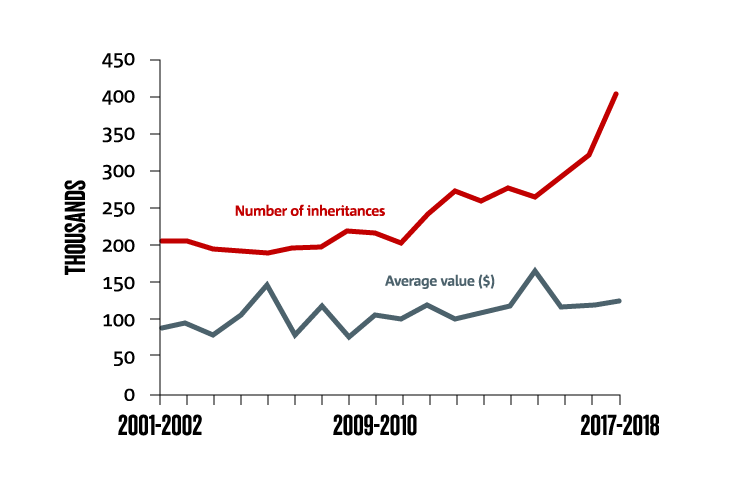

The average number and value of inheritances received by financial year.

The average number and value of inheritances received by financial year.

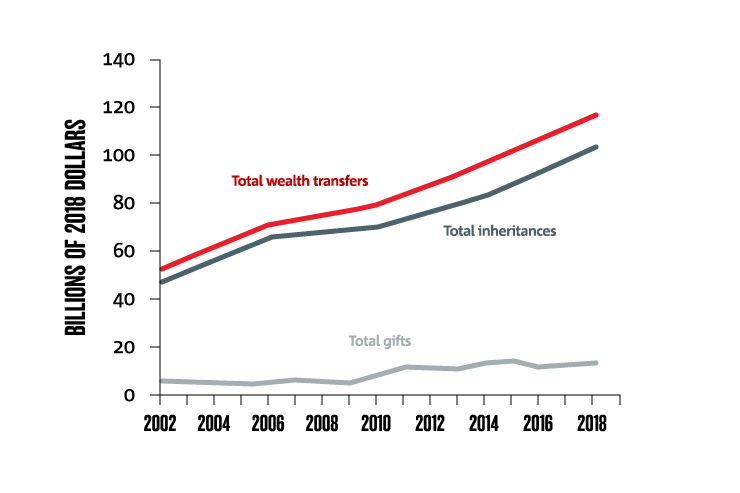

The annual value of wealth transfers has more than doubled since 2002. This is expected to continue to grow, as most retirees do not draw down significantly on their superannuation savings. In fact, 40% have more money at death than they did at retirement.

The annual value of wealth transfers has more than doubled since 2002. This is expected to continue to grow, as most retirees do not draw down significantly on their superannuation savings. In fact, 40% have more money at death than they did at retirement.

Building strong foundations

So, what factors make transferring wealth a success?

“Good communication is everything,” Senior JBWere Adviser Nicole Price says. “Having those candid conversations that mean everyone understands what you want to achieve. There will be a lot less angst that way.”

Before you make any specific promises, however, ensure you and your partner agree. “It’s hard to get the genie back in the bottle once it’s out,” Price warns.

To ensure your ambitions can be achieved, you also need genuine engagement and a decision-making process where everyone moves forward together.

The bigger and more complex your family, the more important this becomes. As JBWere Head of Family Advisory and Philanthropic Services Shamal Dass says, it’s about good family governance – putting in place the processes and structures needed to communicate and make decisions together.

“This ensures that your entire family is on the same page, with a shared vision and path, based on open, honest and informed discussions,” Dass says.

Outside help may assist. In fact, it’s never too early to surround yourself with experts, whether lawyers, accountants, bankers or investment specialists. That way you have all the support you need to make the best decisions from the very start.

Passing on the family business

A fair, frank and collegial approach is especially important when transferring a family business.

“Often, the family business is the largest asset and difficult to divide,” Price says. “If the intention is to retain it, it’s hard to strike a fair balance among children if only some are active in the business.”

This becomes more problematic as families mature and grow. “The reality is, not everyone will want to participate,” Price says. “Issues of equity will arise when the business is where the wealth is.”

This makes it critical that each family member has their say. You also need to understand what each member can bring to the table so you can decide how best to move forward with everyone engaged.

Once you know which siblings are interested in taking on the family business, you need to work out whether they have the capacity to do so. This is best done early so, if necessary, this person can develop the missing knowledge and leadership skills.

If one person wants to take charge, you should consider whether the other siblings continue as shareholders, then discuss how to balance their interests with whoever is managing the company.

If no-one is interested in taking on the business, consider winding it up or selling it. Ultimately, this may do more to preserve your family’s wealth and harmony.

Using your wealth to help create change

You’ll also want to be upfront about your philanthropic goals, to help ensure your wealth is passed down meaningfully.

“Clients with wealth may choose to foster a culture of giving in their family and will do this in their lifetime by setting up an ancillary or ‘giving’ fund,” Price says. “I have clients who transfer some wealth in their lifetime into charitable funds to drive conversations annually on the distribution of the income and causes they support.”

Stating your goals is particularly important, given the amount of wealth soon to be transferred. This represents a unique opportunity to contribute to change that improves the lives of many, including your family.

But only if it’s done well. “When you’re dealing with complex matters like addressing inequity and inequality, you’re really investing in creating a better society and environment in which you, your family and those around you can thrive,” Dass says. “So it’s very important that family patriarchs and matriarchs not only know what they want to achieve as individuals, but also what it is that their family wealth can achieve as a whole.”

Giving early

It may be that you won’t want to wait until your death to transfer wealth to family members.

Many Australians are opting to bankroll the purchase of a new home or the education of grandchildren. What’s more, the inheritors of wealth are often expected to do the same.

However, it should never be viewed as a ‘must’, warns Price.

In fact, she has found that most clients prefer to remain the custodian of their wealth - with good reason. A gift can leave you vulnerable at the end of the day. “Once given, it can’t be returned, so it’s important to be certain it won’t leave you financially insecure,” Price says.

The freedom to choose

Also be prepared for the fact that whatever your ideas around the transfer of wealth, those receiving it may have other thoughts on how your money should be spent – and that may not necessarily be a bad thing. None of us can assume the pathway for the next generation, who will bring their own ideas and values to how they manage inherited wealth.

Says Saadie, “we want to start having conversations with these families and business owners now, to best support with this shift. What are your intentions? Is it philanthropy? Is it community? Is it about how can we support the next generation? “What do you want from wealth?”. This makes it all the more important to put in place the structures that will give your family the freedom to tread its own path well and, in so doing, potentially help the largest ever transfer of intergenerational wealth shape Australia for the better.

Contact our team for personalised lending, investment and advice solutions to help enhance your wealth and secure your future.

When it comes to managing their wealth, the younger generation are doing it differently. Find out how in Part 2 of our Future Focus series.

Terms and Conditions

Apologies but the Important Information section you are trying to view is not displaying properly at the moment. Please refresh the page or try again later.

The information contained in this article is gathered from multiple sources believed to be reliable as of the end of July 2023 and is intended to be of a general nature only. It has been prepared without taking into account any person’s objectives, financial situation or needs. Before acting on this information, NAB Private Wealth is a division of National Australia Bank Limited ABN 12 004 044 937 AFSL and Australian Credit Licence 230686 (NAB) and JBWere Limited ABN 68 137 978 360 AFSL 341162 (JBWere) recommend that you consider whether it is appropriate for your circumstances. NAB and JBWere recommend that you seek independent legal, financial and taxation advice before acting on any of this information.

Wealth advice services are provided by JBWere which is a wholly owned subsidiary of NAB.

JBWere’s obligations do not represent deposits or other liabilities of NAB. NAB does not guarantee its subsidiaries’ obligations or performance, or the products or services its subsidiaries offer. You may be exposed to investment risk, including loss of income and principal invested.

Information correct as at March 2023.

©2023 NAB Private Wealth is a division of National Australia Bank Limited ABN 12 004 044 937 AFSL and Australian Credit Licence 230686. ©2023 JBWere Limited ABN 68 137 978 360 AFSL No. 341162.